Economic Development Should Not Be Confused With Economic Growth

As currently defined, the term economic development is often conflated with

development and growth, which adds to confusion in both policy and academic debates. A

careful contrast between the two, however, is instructive. Economic growth has a strong

3

theoretical grounding and is easily quantified as an increase in aggregate output. In theorizing

economic growth, David Ricardo (1819), and later Robert Solow (1956) and many others

conceptualize an economy as a machine that produces economic output as a function of inputs

such as labor, land, and equipment. Output can increase either when we add more inputs or use

technology or innovation in order to enhance the efficiency with which we transform inputs into

outputs. Subsequently, growth occurs when output increases. In part because of this

straightforwardness, economic growth dominates the debate, with its emphasis on increases in

population, employment or total output, despite the fact that increases in any or all of these could

be associated with both improvements and/or declines in prosperity and quality of life.

Regarding the latter terms, the consensus is that development is a fuzzier and more far-reaching

idea.

Nobel laureate Robert Lucas (1988:13) quips, “we think of (economic) growth and

(economic) development as distinct fields, with growth theory defined as those aspects of

economic growth we have some understanding of, and development defined as those we don't.”

Economic growth is easily quantified and measured, while economic development is

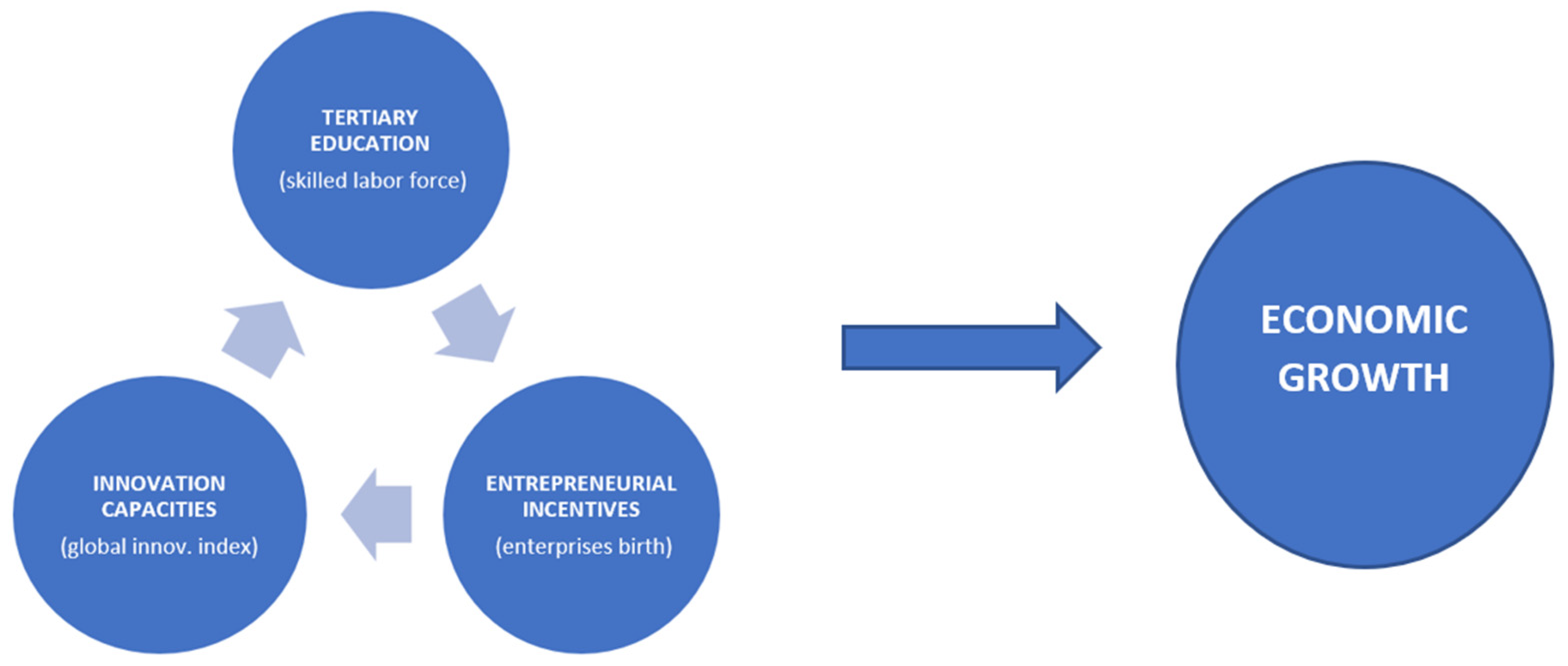

more qualitative and “has meant all things to all men and women” (Arndt 1987:6). Economic

development is focused on quality improvements, risk mitigation, innovation, and

entrepreneurship that place the economy of a higher growth trajectory. While economic growth

is tied to macroeconomic conditions and a function of market forces, economic development

represents the conditions that determine the microeconomic functioning of the economy,

affecting both the quality of inputs and the opportunity set for firms.

Economic development is

associated with institutions, social capital, labor and capital mobility, and income and wealth

equity (Fagerberg et al. 2013).

Gordon (2010) argues that current productivity rates represent the slowest growth in

measured American living standards over any two-decade interval recorded since the

inauguration of George Washington, and Cowen (2011) describes the last several decades as “the

Great Stagnation.” There is clear cause for concern: since 1973, growth in productivity has been

lagging compared to historic rates, except for periods leading up to economic bubbles. This

suggests that macroeconomic policy has not been able to engineer a solution. By focusing on the

microeconomic foundation of the economy, economic development offers perhaps the best, and

maybe the only, policy prescription for sustainable economic growth.